The modern era of transparency at the U.S. Federal Open Market Committee (FOMC) was ushered in by the late Dr. Alan Greenspan. Greenspan led the FOMC and shaped economic policy thinking in the U.S. since the Nixon Administration.

Heavily influenced by Libertarian Ayn Rand’s laissez-faire capitalist approach, Greenspan was credited with supporting an unprecedented growth in the U.S. economy. He was also criticized for policies that created the housing bubble that led to the 2008 Great Financial Crisis (GFC).

Policies of expanding the FOMC balance sheet were picked up by Ben Bernanke’s helicopter money solutions.

As the first chart shows, the huge expansion of the FOMC balance sheet started after the GFC under Bernanke, but Greenspan started it with co-ordinated global central bank rate moves in 1998 and zero interest rate policies after the Dot Com bubble burst and 9-11 hurt the global economy.

Today, the new FOMC leadership seems to be moving to less transparency, and a better “task force” like economic analysis to aid in monetary policy transmission.

Greenspan started at the FOMC in an era of productivity growth, increased globalization, and a peace dividend as the Berlin Wall came down that was very disinflationary and did not have to worry too much about inflation. Today’s FOMC has massive debt, deficits, unfunded fiscal obligations, poor demographics along with artificial intelligence (AI) that could displace a massive percentage of the workforce.

Less globalization and an increased spending of defence to protect the world are likely inflationary trends and detracting from more productive growth investment.

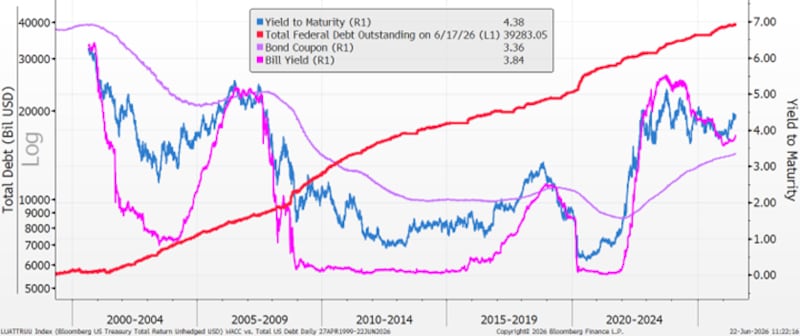

We have noted that the total cost of funding the U.S. debt is a massive part of the new co-operation between the FOMC and U.S. Treasury. This new FOMC path should make the bond market more volatile but should also help keeping the cost of debt finance under control.

At some point, it will matter for equity valuations that have been boosted by the massive AI investment keeping earnings and the economy pumping.

Follow Larry

YouTube: LarryBermanOfficial

LinkedIn: LarryBerman